There’s a fascinating story in today’s Cavalier Daily that brings to light what has previously been discussed here on RealCentralVA – but this time with more data substantiating their claims:

“Obviously you see the headlines of [areas] that have drastic numbers of foreclosures,†Lovelady said, noting that it is “easy to think of Charlottesville as isolated from this.â€

Lovelady said Charlottesville is not isolated from the foreclosure crisis, especially when considering issues such as neighborhood foreclosures.

…

The group that studied the topic of forecasting foreclosures saw several trends, including an 89-percent increase in foreclosures since 2006, the fact that 56.8 percent of foreclosed loans are adjustable rate mortgages and that 62.5 percent of home loans in Virginia are adjustable rate mortgages, Bridger said. Some financial analysts have argued against adjustable rate mortgages, noting that some consumers who enter into a low interest rate loan later find themselves unable to repay the loan should the interest rate rise.

“The good news is that the number of ARMs and subprime loans originating is decreasing, but many of them are soon to reset,†Bridger said.

(bolding mine)

As noted in June 2008–

We may not have seen the worst of what this cycle has to offer. I believe that the bulk of short-term ARMs have not yet reset, and until this happens (likely in 2009 and 2010) we may not see the proverbial “bottom.’ That being said, we won’t know the bottom until we have the benefit of nine to eighteen months of hindsight.

I would love to see a copy of their presentation as well as the underlying data (and am waiting on a response), especially because this appears to be the first, best and most localized foreclosure study on the Charlottesville area. Trend lines, breakdown by zip code/neighborhood/street/school district – all of this would be helpful for Realtors and the public to get a better handle on what exactly is happening in our market.

There is no good data source for accurate and timely foreclosure information in the Charlottesville, Virginia area. Witness:

Trulia lists four active foreclosures.

My IDX site shows three active foreclosures. (although this is a beta feature)

Foreclosure.com shows nine foreclosures, one foreclosure and 24 bankruptcies.

Hotpads shows seven foreclosures.

No wonder no one has any real idea as to what’s going on – with inaccurate and incomplete data, we’re left to making educated guess and speculation.

Add to all this that 3rd Quarter mortgage delinquencies “shot up in the third quarter from the same period last year …” (hat tip: Agent Genius)

Update 18 December 2008:

Search for Charlottesville/Albemarle Foreclosures here; this is not all of the ones in the Charlottesville area, but a pretty good starting point.

.

Jim,

I too would love to see the presentation. Perhaps CAAR would allow them the space to present to the Realtor community if they would be willing to.

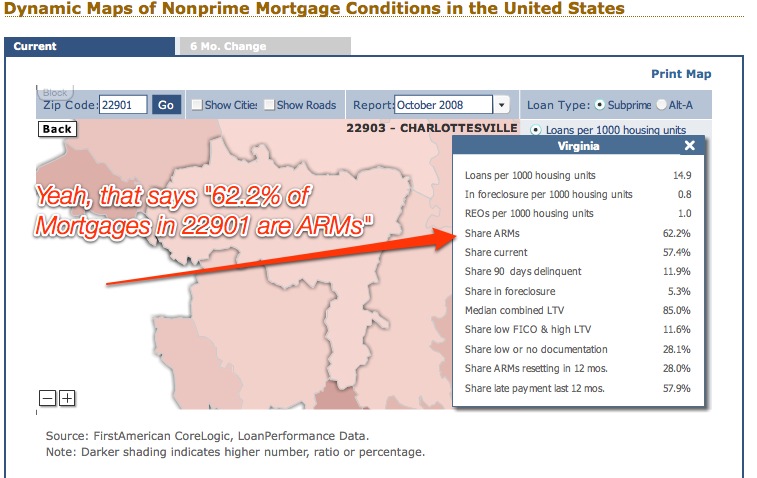

However, I don’t understand the graph you show. I went to the F.A. web site to try and re-create it, but with no luck. I don’t believe that 65% of loans can be ARMs. If you told me that 65% of loans originated since 2002 were ARMs I might believe you, but not the total market.

More importantly, that graph states that 0.14% of homes in 22903 have mortgages on them. If that is true that 99.86% of our neighbors have no mortgages, then we are not going to have a foreclosure issue.

Also, they show REOs at a full 1% yet in the process foreclosures at 0.8%. Would it be possible to have more homes bank owned already than are in the process of becoming bank owned? I guess it’s possible, but I would think that the auction world could take care of that pretty darn quickly if the banks wanted them to.

If this graph is really accurate (and it could very well be that I just don’t understand some of the presentation), what scares me is that not even 60% of our mortgage holders are current on their mortgages. Yikes!

Keith –

I just went to the site and typed in 22901 and that popup showed; I suspect that they, like many, use 22901 as a catch all for “Charlottesville.”

As far as banks “wanting them to” – I’m still under the impression that many banks/REO companies are reluctant to reduce prices to where they truly need to be – although I would love to be corrected.

Lastly, I would not be surprised if more than half of the mortgages in “Charlottesville” (CharlAlbemarle at the least) were short-term ARMs – and this bodes ill for the future for sellers but presents potentially tremendous opportunity for buyers/investors.

Foreclosures soared in Q3 according to TransUnion:

https://tinyurl.com/5nvdkb

Resetting Alt-A and Prime loans, and the potential FHA “subprime” debacle will all cause market turmoil in the coming months–or years.

https://www.msnbc.msn.com/id/27844894/#storyContinued

You may still find Option ARMs as mortgage choices on the websites of local banks, fwiw.

If buyers and investors can get “good deals” out of the coming chaos, it will be a blessing, as the wife says. Otherwise, it’s just going to be a debacle for America.