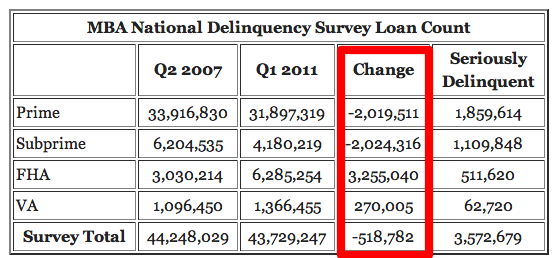

I found the above chart from Calculated Risk fascinating.

If you’re a consumer/homeowner (and voter) you should pay attention. People who likely understand this stuff less than we do (politicians) and who probably won’t read the relevant bills are likely going to be making incompetent decisions that affect all of us. As always, there is a likely a middle ground between the lobbyists (NAR) and the government (who seemingly have no desire to actually fix the problems, just to curry favors and win re-elections).

Briefly: sea changes in the lending environment are in the offing. Proposals range from forcing lenders to have skin in the game to requiring many/most buyers to put down 20% downpayments – this would affect buyers, sellers, real estate agents (like me), all the ancillary professions and the entire American economy.

Educate yourselves; I’m trying to do so myself.

QRM:

I touched on this a few weeks ago:

4a – QRM becomes law –

The proposal would allow participants to avoid the 5% requirement when they securitize “qualified residential mortgages (QRM),” deemed relatively safe from default by borrowers. To fit this category, a mortgage would require a borrower with a solid credit rating who will make a down payment of at least 20%. Studies have shown that borrowers are less likely to default if they have made large down payments, which represent equity that would be lost in a foreclosure. Many of the bad loans issued a few years ago required little or no down payment.

4b – I know I’m simplifying this, but if a buyer is required to have some skin in the game, why shouldn’t the lender? From the NAR:

NAR also has concerns about the proposed risk retention regulation under the Dodd-Frank Act that requires lenders that securitize mortgage loans to retain 5 percent of the credit risk unless the mortgage is a qualified residential mortgage (QRM). High down payment requirements are being proposed by federal regulatory agencies as part of the QRM exemption. Most Americans still consider having enough money for down payment and closing costs to be the biggest obstacles to buying a home. According to NAR estimates it could take as many as 14 years for the average family to save for their down payment. Higher down payments do not have a meaningful impact on default rates; NAR supports a reasonable and affordable cash investment requirement coupled with quality credit standards, strong documentation and sound underwriting.

4c – Let’s not forget one of the main reasons we got in the mess we were/are in: (I originally noted this in 2007)

The key reason the Subprime problem exists as it does today has to do with the wanton disassociation of risk inherent in the machine that churns out Subprime loans. Unlike the S&L crisis of the 1980s, the mortgage lenders of today aren’t taking their own balance sheet risk when underwriting loans. These brokers get paid for quantity REGARDLESS of quality. The balance sheet risk is transferred through three entities in less than 90 days from origination. The originator will originate ANYTHING he can sell to a whole loan buyer to pass the hot potato on. Whole loan buyers are simply the aggregators of loans at the Wall St. firms that aggregate, package, tranche, and sell as quickly as they possibly can to the clueless buyer. This transference of risk is the crux of the Subprime situation. Just think about it…if you were a 20-something making mortgage loans in California using someone else’s balance sheet and being paid per loan (with no lookback to performance of the loan), how many dubious loans would you underwrite?

ON the other side, Matt said has a very valid point – if lenders are required to hold percentages of loans on their own books, that would likely thin out some of (all of?) the smaller lenders and thus reduce competition for consumers.

Competition is good; so is getting the government out of the lending business.

Related reading:

– The KCM Blog folks say that “QRM just doesn’t make sense.”

– Qualified Residential Mortgage Regulations Threaten the Housing Market (The Heritage Foundation) – pay attention to the “Preserving Fannie Mae and Freddie Mac and Expanding FHA” section.

– Op-Ed: Impeding Availability of FHA Financing Would Be a Setback for Homebuyers

– When it comes to loan quality, down payment doesn’t matter

This post is a continuation of the Sunday radio conversation on WNRN, podcast hosted by Cville Podcast. It was a really good conversation, and I highly recommend listening.