What is happening, what is about to happen, and more importantly, what will the impact be on the Charlottesville area real estate market? If there was some way that I could determine and assess what percentage of loans written in the Central Virginia area were subprime, then that analysis would be far better, so all I have to run with is my anecdotal evidence. As far as I know, I have not represented a buyer who has purchased a home using a sub-prime mortgage. Nor have I represented a seller who accepted an offer based on a pre-approval that indicated or alluded to a subprime product being used.

Consider this from the WSJ (temp free link):

The housing boom kept loan losses unusually low, because borrowers who got into trouble could easily sell their homes for a profit or refinance into a cheaper mortgage. Many “subprime” borrowers (people with weak credit records) bought homes with no down payments. More than 40% of subprime borrowers last year weren’t required to produce pay stubs or other proof of their income and assets, according to Credit Suisse Group. At the same time, some lenders have become more reliant on computer models to estimate the value of homes.

“We’re not really sure what the guy’s income is and…we’re not sure what the house is worth,” says Mr. Ranieri, who now runs his own investment businesses in Uniondale, N.Y. “So you can understand why some of us become a little nervous.” (bolding mine)

The shakeout of the subprime market could have profound implications on the entire real estate market, the mortgage market and many of the ancillary businesses.

Who was looking out for those who took the subprime loans? Should there have been anybody “looking out” for these people, or should they be solely responsible for their decisions? What about the shareholders and employees of the companies who were recklessly writing these loans?

Will there be a lot of short sales that will both present opportunities to those who are positioned to take advantage? What might these do to neighbors’ property values?

There are more questions and speculation than answers right now, but there will doubtless be significant and far-reaching ramifications. Frankly, I am sure that this will touch segments of the economy that I, and others, may have never considered. Looking back from a window of five years removed will be interesting.

These are some of the stories I have been reading to help me get a better understanding:

Foreclosures: “At the beginning of this cycle” (Calculated Risk)

Could Tremors in the Subprime Mortgage Market Be the First Signs of an Earthquake? (Wharton)

NovaStar Financial Share Prices Rocked By Earnings Report (Real Estate bloggers)

Seeking Alpha

Block’s Blocked with this telling paragraph that to me simultaneously describes and indicts the entire segment:

Block chased borrowers who shouldn’t have been borrowing right along with the rest of subprime lenders. The whole category is tatters these days, with defaults for the industry up and several lenders going bankrupt. (bolding mine)

CNN

Group sees spike in subprime mortgage foreclosures (MSN)

Subprime woes (WSJ)

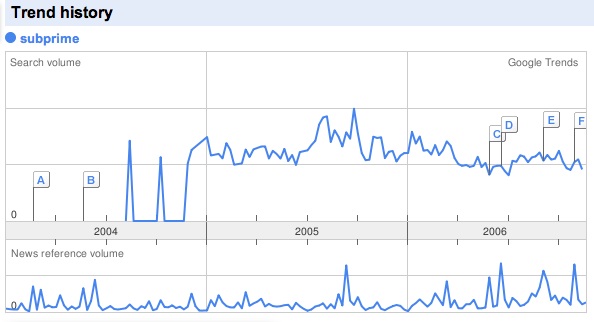

I am waiting for the spike in this Google Trends graph:

*I am not an economist.

Technorati Tags: mortgages, subprime, real estate

Subprime will probably do the most damage in L.V. During their run-up (driven by people escaping from California) there were a lot of these “alternative loans” fueling their housing boom.

Now they’re starting to feel the heat

Earlier this month:

Too bad I’m not going to be in a place where I can take advantage of it.